Introduction

In the realm of financial planning and retirement security, income annuities have long been a cornerstone for those seeking stability and predictability. As we navigate through a landscape marked by fluctuating markets, uncertain economic forecasts, and growing geopolitical tensions, the appeal of income annuities has become increasingly pronounced. The current financial landscape, characterized by the highest interest rates seen in 15 years, presents a unique and compelling opportunity for those considering income annuities.

An income annuity is a contract with an insurance company, crafted to provide a reliable stream of income, often lasting a lifetime. This financial instrument has been a vital part of retirement planning for those seeking a safeguard against the unpredictability of market-based investments.

The surge in interest rates is particularly significant for income annuities. Higher interest rates typically translate to more favorable annuity payout rates, making this an opportune moment for potential investors. In this article, we will explore the intricate relationship between rising interest rates and the advantages of income annuities. We’ll discuss how these conditions create a favorable environment for guaranteed income, potential inflation adjustments, and tax efficiencies, making now an ideal time to consider an income annuity as part of your retirement strategy.

Understanding Income Annuities

Income annuities are a type of financial product offered by insurance companies, designed to provide a steady stream of income, typically for the rest of the annuitant’s life. They are particularly popular among retirees and those nearing retirement age, as they offer a predictable income source independent of market fluctuations. Understanding the basics of income annuities, including the different types available, is crucial for making informed financial decisions.

Definition of Income Annuities

At its core, an income annuity is a contract between an individual and an insurance company. The individual pays a lump sum or a series of payments to the insurer, and in return, the insurer agrees to make periodic payments to the individual for a specified period or for life. This arrangement provides a reliable income stream, offering peace of mind and financial stability, particularly in retirement.

Types of Income Annuities

There are two primary types of income annuities: immediate and deferred.

- Immediate Income Annuities: As the name suggests, immediate income annuities start paying out almost immediately after the initial investment. Typically, payments begin within a year of purchasing the annuity. This type is ideal for individuals who are already retired or are very close to retirement and need an income source right away. The payout amount depends on several factors, including the lump sum invested, the annuitant’s age, and the prevailing interest rates at the time of purchase.

- Deferred Income Annuities: Deferred income annuities, on the other hand, involve a waiting period before the payments start. This period can range from a few years to several decades. The primary advantage of this type is that it allows the investment to grow over time, potentially leading to higher periodic payments in the future. Deferred annuities are suitable for individuals who are still in the workforce but want to secure a steady income stream for their retirement years. The longer the deferral period, the larger the eventual payouts can be, due to the accumulation of interest and the shorter expected payout period.

How They Work

The mechanism of both immediate and deferred income annuities is based on the principles of risk pooling and time value of money. When you purchase an annuity, your investment is pooled with funds from other annuitants. The insurer then uses this pool to make periodic payments to annuitants. Actuarial science helps insurers predict life expectancies and calculate payment amounts to ensure the sustainability of the annuity fund.

Income annuities offer a way to convert a portion of your savings into a guaranteed income stream, providing financial certainty in an uncertain world. As such, they play a pivotal role in many retirement planning strategies. Understanding the distinctions between immediate and deferred income annuities is essential for choosing the option that best aligns with your financial goals and retirement plans.

Current Market Advantages

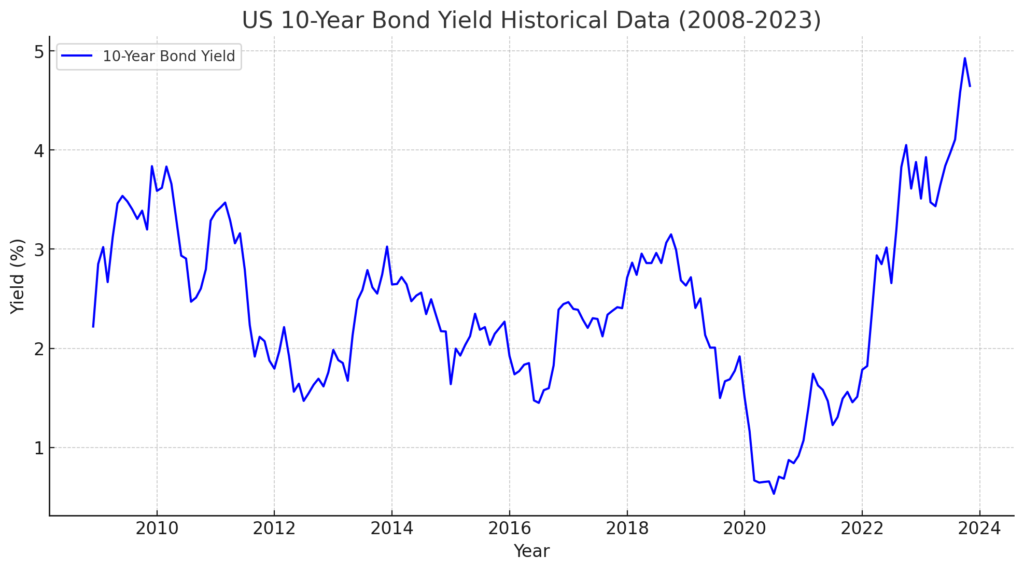

In the past 15 years, the US 10-Year Bond Yield has experienced considerable fluctuations, reflecting changes in the economic landscape. The yield reached its peak in October 2023, hitting 4.926%, the highest in this period. This peak is particularly notable when considering the average yield over these 15 years, which stood at around 2.40%.

Data Source - United States 10-Year Bond Yield Historical Data

The significance of this recent surge in bond yields cannot be overstated, especially in the context of income annuities. Higher bond yields generally lead to better annuity rates, as insurance companies can earn more on their fixed-income investments. This correlation means that the current high-yield environment is particularly advantageous for those looking to invest in income annuities. The increased yield offers more attractive payout rates for new annuity contracts, making it an ideal time for potential investors to lock in these rates.

This data provides a compelling backdrop for understanding the current attractiveness of income annuities. With bond yields at a 15-year high, the financial environment is ripe for those seeking to secure a stable and potentially more lucrative income stream through annuities.

Current Payout Rates for Immediate Annuities

Lets take a look at a real-world example using today’s current rates.

Immediate annuity payout rates are determined by many factors, including the premium amount, payout length, age of the annuitant, and current rates set by the insurance companies. This example is using the parameters of a 60 year old investor with $250,000 in premium with a guaranteed lifetime payout.

This information is not a quote, contract or guarantee of future performance. It is for comparison and informational purposes only.

Current Payout Rates for Deferred Income Annuities (Income Starting in 5 Years)

In this example provided, we look at a deferred income annuity for a 60-year-old male who invests $250,000, with income starting in 5 years.

Investment and Payout Details:

- Initial Investment: $250,000

- Income Start Age: 65 years old (5 years after the initial investment)

- Annuity Type: Deferred Income Annuity

Payout Information:

At the age of 65, the annuity begins to pay out. The payout rate is calculated based on the accumulated value of the annuity at the time of activation. For this example, the payout information is as follows:

- Year 1 to 4 (Age 60 to 63): No payouts as the annuity is in the accumulation phase.

- Year 5 (Age 64): The accumulated value of the annuity is $217,375.

- Lifetime Withdrawal Rate: 7.77%

- Annual Payout Starting at Age 65: $27,500

This payout represents the amount the annuitant will receive annually, starting at age 65. It’s important to note that the actual payouts may vary based on the performance of the annuity’s underlying investments and other factors.

Break-Even Analysis

To understand the break-even point, we need to calculate how long it takes for the total payouts to equal the initial investment. In this case, the initial investment is $250,000, and the annual payout is $27,500.

Based on the given example, it would take approximately 9 years for an investor to reach the break-even point with a deferred income annuity. This means that after age 74, the total amount received in annuity payments would equal the initial investment of $250,000.

Current Payout Rates for Deferred Income Annuities (Income Starting in 10 Years)

This section will explore the payout rates for a deferred income annuity based on an example where the income starts in 10 years for a 60-year-old who invests $250,000.

Example Overview:

- Initial Investment: $250,000 at age 60.

- Income Start Age: 70 (10 years after the initial investment).

- Annual Payout: Starting at age 70, the annual payout is $41,682.

Payout Analysis:

- After a 10-year deferral period, the annuity starts paying out an annual amount of $41,682 at the age of 70.

- This example demonstrates the impact of a longer deferral period on the payout rate. The longer the money is invested without withdrawal, the higher the eventual payout becomes due to the accumulation and compounding of interest.

This payout represents the amount the annuitant will receive annually, starting at age 70. It’s important to note that the actual payouts may vary based on the performance of the annuity’s underlying investments and other factors.

Break-Even Analysis

To understand the break-even point, we need to calculate how long it takes for the total payouts to equal the initial investment. In this case, the initial investment is $250,000, and the annual payout is $41,682.

Based on the given example, it would take approximately 6 years for an investor to reach the break-even point with a deferred income annuity. This means that after age 76, the total amount received in annuity payments would equal the initial investment of $250,000.

Longevity and the Increasing Benefits of Income Annuities

One of the most compelling features of income annuities is their ability to provide financial security that grows more advantageous with age. As these products guarantee income payments for life, their value increases significantly the longer you live. This aspect makes them especially beneficial for those who enjoy longer than average lifespans, ensuring a steady stream of income well into advanced age.

Impact of Longevity on Payouts

Let’s consider the total payouts from different types of annuities when the investor reaches the age of 85:

-

Immediate Annuity: An investor who starts receiving payments immediately from an annuity at age 60 would have received a total of $454,871.75 by the age of 85. This scenario underscores the advantage of a continuous payout over a long period.

-

Deferred Income Annuity (5-Year Deferral): In the case of an annuity with a 5-year deferral period, the total payout by age 85 amounts to $550,000. This higher total reflects the deferred nature of the annuity, where payouts start later but accumulate rapidly.

-

Deferred Income Annuity (10-Year Deferral): For an annuity with a 10-year deferral, the total received by age 85 reaches $625,230. This example demonstrates the significant benefit of a longer deferral period, offering the highest total payout among the scenarios.

Additional Benefits: Nursing Home Riders

Many deferred income annuities offer an added layer of security through nursing home riders. These riders are designed to address the increased financial needs that can arise from health-related changes in later life. If the annuitant needs to enter a nursing home, these riders typically double the payout amount, providing additional financial resources during a time when they are most needed. This feature not only enhances the annuity’s value in providing for long-term care needs but also offers peace of mind in planning for unforeseen health expenses.

Conclusion:

As we have explored in this article, the current financial climate, marked by high-interest rates and economic uncertainty, presents a compelling case for investing in income annuities. Whether it’s an immediate annuity for those seeking immediate income post-retirement or a deferred annuity for those planning ahead, the advantages are clear and significant.

The longevity aspect of income annuities cannot be overstated. As we live longer, the need for a reliable, lifelong income stream becomes increasingly critical. Income annuities meet this need effectively, providing financial security that grows more valuable the longer you live. The examples we discussed illustrate how these products can deliver substantial total payouts, particularly for those who choose to defer their income.

Moreover, the inclusion of features like nursing home riders in many deferred income annuities adds an additional layer of security, ensuring that if health needs change, financial resources can adapt to meet these challenges.

In conclusion, income annuities stand out as a prudent choice for anyone seeking a stable, guaranteed income stream in retirement. With their ability to provide financial peace of mind, adapt to changing life circumstances, and offer significant payouts over time, income annuities are more than just a retirement planning tool—they are a cornerstone for a secure, comfortable, and resilient financial future.

As with any financial decision, it is advisable to consult with a financial advisor to ensure that an income annuity aligns with your individual goals and circumstances. In these times of economic flux, securing a stable income for the years to come is not just a comfort—it’s a strategic move towards a more secure retirement.

Use The Annuity Quote Calculator to run a custom illustration of today’s top income annuities