Understanding Fixed Indexed Annuity Crediting Methods

There are many variations of fixed indexed annuity crediting methods available. It can be difficult to figure out which is best to choose when purchasing an annuity. Although annuities are typically fairly simple products, the indexing methods can be a spot of confusion. In this article, we will attempt to explain the basic terms and methodologies behind the different crediting options within indexed annuities.

Fixed Indexed Annuities have certain components that help determine how much indexed interest you can receive in a given year.

Some annuities have only one component, other annuities may have several. These are the most common fixed indexed annuity components:

Fixed Indexed Annuity Caps:

Many indexed annuity contracts set a “cap,” or a maximum interest rate the annuity can earn in a given period. If the return of the index you select exceeds the cap, the cap is used to calculate your interest.

For example, if the annual cap in this hypothetical example were 4% and the value of the index rose by 7%, the cap amount of 4% would be credited to your contract. However, if the index change was 2%, your contract would be credited 2%, since that is lower than our hypothetical cap.

Fixed Indexed Annuity Participation Rates:

In some annuities, a participation rate determines what percentage of the index increase will be used to calculate your indexed interest. For example, let’s suppose that the index rose by 7%. If a hypothetical indexed annuity had a 50% participation rate and no other reducing component, the contract would receive 3.5% in indexed interest.

Fixed Indexed Annuity Spreads:

In other cases, the indexed interest rate credited is determined by subtracting a spread from an index’s gain during a specified period. This is known as a spread.

For example, if the index increased by 7% and your hypothetical annuity had a 5% spread, your indexed interest would be 2%. If the index only gained 2% for the year, the amount of the gain (2%) is less than the spread (5%), so no indexed interest would be credited.

Crediting Methods

Annual Point-to-Point:

This is the simplest of the crediting methods. Annual point-to-point uses the index value from only two points in time, so it may be a good choice if you want to maximize the effects of mid-year market volatility.

How it works:

- On your contract anniversary, the beginning index value is compared to the ending index value.

- The percentage of change in the index is calculated.

- If the ending index value is higher than the beginning index value, a participation rate, a cap, or a spread is applied to determine the amount of indexed interest you will receive.

- If the value is lower, you won’t receive indexed interest.

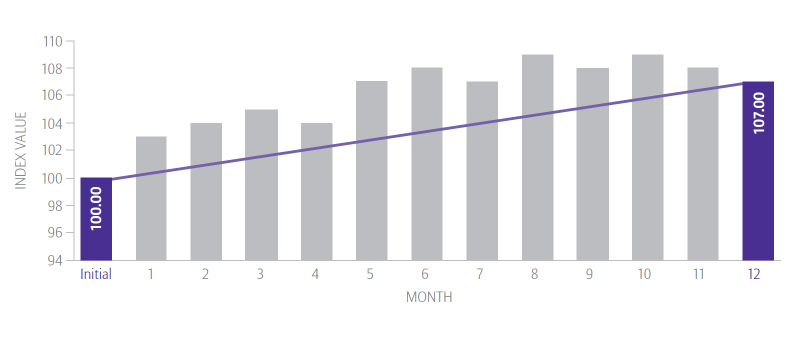

Annual Point-to-Point Example:

In this hypothetical example, the beginning index value (100) is compared to the ending index value (107), resulting in a change of 7%. The actual amount of indexed interest credited could depend on a participation rate, a cap, or a spread.

For example, if the participation rate were 50%, the indexed interest for this contract year would be 3.5% (50% of 7%).

If the cap were less than 7.00%, the interest for that year would equal the cap.

Finally, if this hypothetical example had a 5% spread, the indexed interest would equal 2% (7% change in index value – 5% spread = 2% indexed interest.

If the final result is negative, no indexed interest would be credited and your contract value would remain unchanged.

Monthly Sum:

Monthly sum is the most volatility-sensitive crediting method. It can provide interest in steady “up” markets, but it can be adversely affected by large monthly decreases.

How it works:

- On the contract anniversary each month, the index value is compared to the prior month’s value, and the percentage of change is calculated.

- At the end of the year, the monthly index increases and decreases are added up. The increases may be subject to a cap; however, decreases are not limited by the cap.

- If the final sum is positive, you’ll receive that amount as indexed interest.

- If the sum is negative, you won’t receive indexed interest.

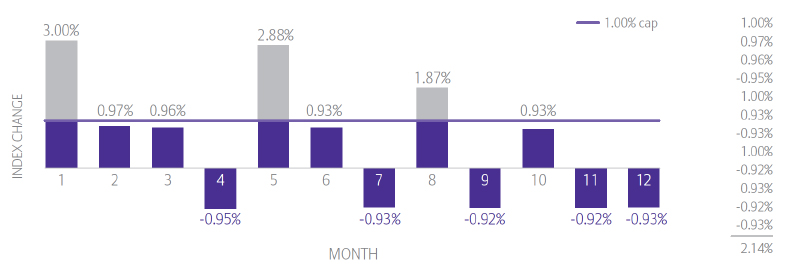

Monthly Sum Example:

This hypothetical example shows a monthly sum crediting method with a sum of 1%.

Every month, the index value is compared to the prior month’s value. The percentages you see above represent the percentage in the index change, month-over-month.

At the end of the year, the monthly percentages are added up. In this example, the contract owner would receive 2.14% in indexed interest.

If the final result is negative, no indexed interest would be credited and your contract value would remain unchanged.

Monthly Average

Monthly average can help reduce volatility by averaging monthly highs and lows over the course of the year. It may be a good choice in turbulent markets.

How it works:

- The index values at the end of each month are tracked for one year.

- At the end of the year, those index values are added together and then divided by 12 to determine the monthly average.

- The starting index value is subtracted from the monthly average, and the result is divided by the starting index value.

- If the final result is positive, a participation rate, a cap, or a spread is applied to determine the amount of indexed interest you will receive. If the final result is negative, you’ll receive no indexed interest.

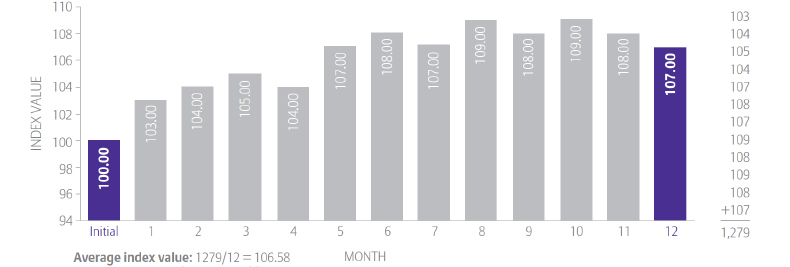

Monthly Averaging Example:

This hypothetical example shows monthly average crediting, with a spread of 5%. In this example, the contract owner would receive 1.58% in indexed interest (6.58% indexed change – 5% spread = 1.58% indexed interest.

If the final result is negative, no indexed interest would be credited and your contract value would remain unchanged.